< GO BACK

How to Introduce “Unreasonable Hospitality” Into Banking

August 3, 2025

/

GENERAL

My “banking mind” is often wired somewhat differently. I wanted to explore whether a universal, retail-focused bank on a digitized incumbent path could drastically increase client trust, cement customer stickiness, and reshape its brand—not just through app features and rates—but through genuine, efficient, no-frills care of the kind seen in top-tier hospitality. In a world where banks race to catch up with disruptors through faster apps, AI-driven re-engineering, and sleek interfaces, something seems missing to me: deep emotional connection. That connection drives long-term loyalty and resilience in a bank’s future operating model. Achieving this requires extending the service portfolio well beyond traditional banking—even beyond embedded finance—into emotional loyalty-building moments.

Let’s play with an idea of a somewhat visionary yet grounded hybrid banking concept: digital efficiency blended with emotional intelligence. Inspired by Will Guidara’s book Unreasonable Hospitality, this is not about gimmicks or marketing spin. It’s about building a bank that clients choose to stay with because it sees them, supports them, and genuinely cares. Hospitality and process excellence must not be seen as contradictions—but as complementary drivers of customer loyalty.

Hyper-personalized banking, with one central purpose: increase the loyalty of current clients and attract new ones not through pricing wars, but by making them feel proud—even privileged—to be your client.

One Step Back: Few Simple Facts About the World’s Banking Industry Today

- 2024 banking industry revenues were the highest among all global industry sectors. With ~EUR 4.1 trillion in net sales and ~EUR 1.4 trillion in profits—driven by a EUR 130 trillion increase in global financial assets over six years—these figures surpass every other sector. The free cash flow to equity? EUR 3.6 trillion in just four years.

- But banks don’t create value in the traditional sense. They serve those who do—and those who strive to. Whether helping the educated achieve dreams or the less-educated reach life goals, banks play a support role. Yet investors continue to undervalue the sector. It trades at a ~70% discount to the rest of the economy on both price-to-book and price-to-earnings.

- Why? Investor distrust. Cited factors include intensifying competition, shifting client behavior, tech disruption, and macroeconomic uncertainty. These concerns distill into four strategic fears: a.) Bank clients are less loyal compared to other industries. b.) Bank clients demand seamless tech interfaces and experiences. c.) Banks lag in meeting clients’ full life-journey needs. d.) Macro shifts increase risk, and banks often don’t adapt fast enough.

- Putting aside the fact banks’ essential business models lie on risk mitigation and stepping away from the macro background for a second, it essentially all boils down to securing client loyalty. And loyal customers are those who genuinely like you. But to genuinely like someone, one needs to feel devotion from the other side. In a business sense, true and welcoming hospitality.

Unreasonable Hospitality Bank Concept

What would a bank need to do—concretely—to offer hyper-personalized, “unreasonably” hospitable services, and in turn build a scalable, investor-attractive operating model?

An intentionally oversimplified step-by-step roadmap could look as follows:

- Reset your internal culture: Teach your staff to serve without compromise, putting NPS, CSAT, speed of client’s problem resolution (or any other metric which shows how your clients value your efforts) at top of their KPI list. Example: world’s best neobanks primarily differentiate from the incumbents by the extreme customer centricity, and speed of interaction with the clients; speed assisted, not driven by tech. They don’t over-document before acting - they act and then adapt.

- Leverage data to segment with empathy. Get your data warehouse people, data translators, marketing and BI people to map and understand the existing customer base on a micro-granular level, segmenting customers based on common attributes being age, income, wealth, channel usage, spending habits, financial goals, education level, geography and the most demanding one, psychological profiling. Reward handsomely those clients who take a bit more time to fill-in your psychological profiling app test (there are some awesome tests available out there addressing core personality dimensions). Move beyond “mass segments”—create personas with names, stories, and aspirations.

- Match client aspirations with bank strategy. Assess where you are today. Define future client segments you want to serve—based on lifetime value, strategic fit, and your growth strategy. Make deliberate choices

- Create client-facing tribes/squads across the entire retail front & back end. Think: a.) on-boarders, b.) hospitality providers and c.) complaint-solving empathetic handlers. Use top restaurant logic working role parallels if needed. These squads (tribes) are multidisciplinary teams that blend analytics, business knowledge and marketing/ people communications skills. They share accountability for the final outcome, and that’s hospitality level for every retail client subgroup, measured through delivered or implemented products, services and care initiatives which I describe below. These squads become your internal champion of care.

- Deliver tiered service like hospitality—without the tiered pricing. Basically, let your squads serve these client groups as if they were your 5*, 4* and 3* hotel guests based on your unique segmentation, but gradually with 4*, 3* and low-cost pricing model, because of your relentless pursuit of achieving high quality low cost-to-serve (co-driven by tech) and highest unit economics. Easier said than done, I know. Simple example from the hotel industry: Julius 5* hotel Prague, 5* guest experience at 3* cost.

- Start with the highest-potential pilot segments. Don’t try to serve all at once. Begin with i.e. digitally fluent, mid-income urban professionals as a pilot. They’re open to emotion-driven finance, low-cost to serve, and yield high LTV if emotionally connected. But don’t stop there. For your premium segments, think Tinkoff’s concierge-style services, for other subsegments, Nubank’s “surprise upgrades”, there are examples out there already.

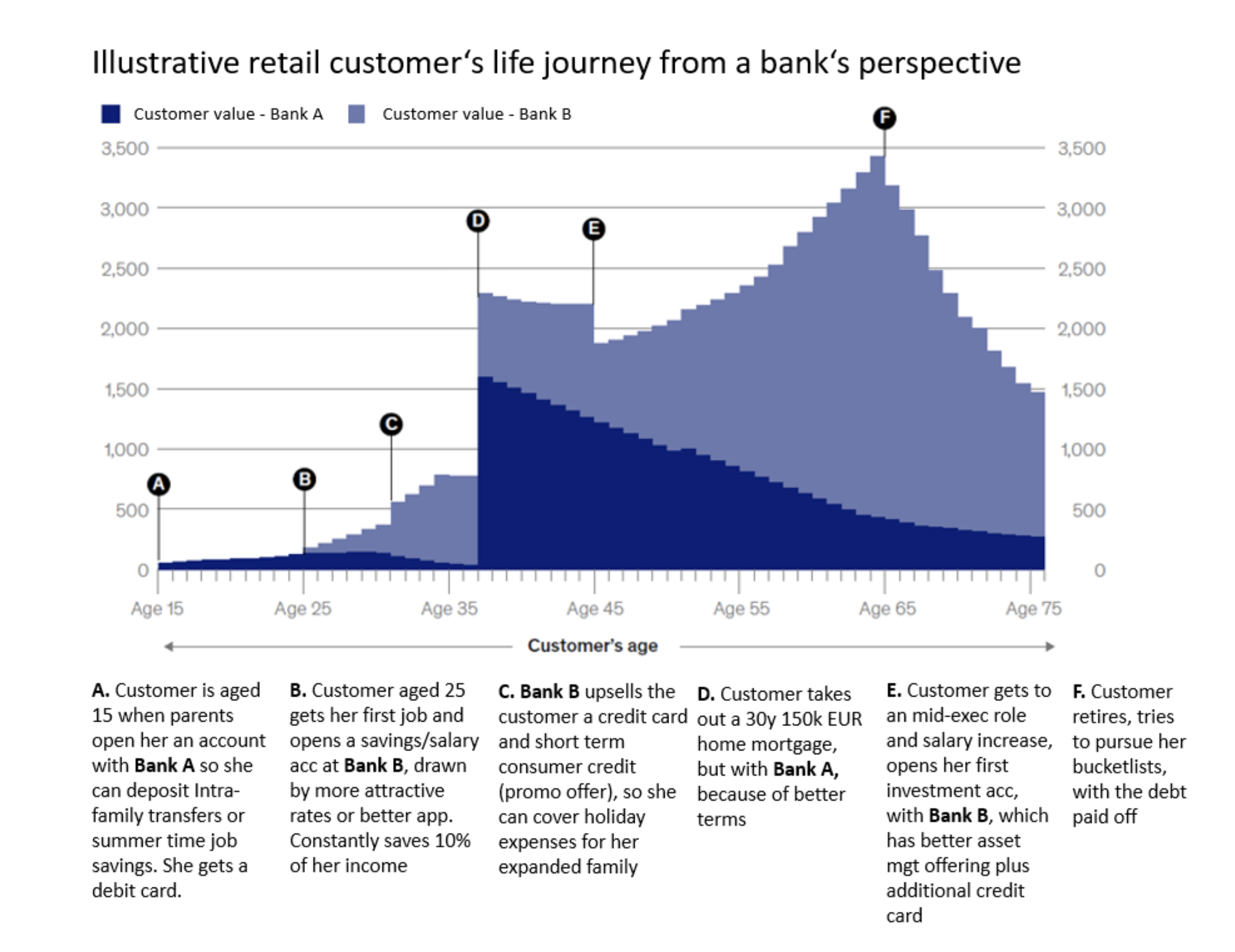

View a typical mid-class college educated client journey through the illustration depicted below (borrowed from McKinsey’s report):

So, what would it take for a bank to avoid the switching and take the entire cumulative value of the client for itself, plus expand it by a whole lot over time, “eating” into the client cumulative LTV serviced by other industries? It could start by introducing true hospitality.

Service and Product Ideas to Support and Introduce Unreasonable Hospitality Concept in Banking

You might call me a dreamer; I won’t blame you. You might wave your hand answering, “give me some Opex estimates behind all that first”, or you might just say “there’s no need for 99% of these ideas, we’re servicing our premium clients well, and we are doing just fine with others as we do the things we do”. But my sole purpose is to stimulate your professional curiosity and awareness that banking is anything but non-emotional intermediation of commodity products, and that every loyal client can be viewed essentially as a premium one.

A: Life Concierge Banking, Reimagined for Scale

Every new client begins with a guided onboarding journey—but not with paper forms. Instead, they’re welcomed by a digital-human hybrid concierge. Example: Just sort of like TymeBank’s onboarding kiosks, offered in both digital and physical formats, blending empathetic human touch with fast digital onboarding.

Selected pre-segmented client groups gain access to concierge service pods—trained teams who offer support around life transitions: first banking experience, moving cities, starting families, changing jobs, retirements. These pods aren’t just for show; they capture emotional and financial signals, making every product recommendation more relevant. Over time, these experiences create emotional switching costs far deeper than standard UX advantages.

B: Modular Account Bundles That Feel Personal

Unreasonable hospitality concept doesn’t offer generic accounts. It offers story-driven bundle accounts tied to your life stage, examples:

- Young earners: we see you got a salary increase, we serve you with habit-saving proposals, housing solutions, investing primers.

- Families: joint accounts, life insurance offers, child savings goals, ticketing, entertainment and travel assistance.

- Career changers: relocation help, tax tools, fee breaks.

There is no such thing as mass client classification anymore, everyone can upgrade her/himself by bundling. Each bundle blends emotion with financial value—and increases clients’ likelihood of staying.

C: The First Salary Promise

You pursue client’s trust. Because once you have that, he/she’ll move his/her income with you. That’s why the concept introduces the First Salary Promise:

“Transfer your salary to our bank and we’ll reward you with 2 surprise upgrades and exclusive Unreasonable Hospitality Circle access.”

It’s not a gimmick. It’s an invitation to build a real relationship. Salary-linked relationships unlock a higher LTV and deeper retention.

D: Hospitality Circles: Deposits That Feel Like Community

You make deposits sticky by making them social. Clients can form Hospitality Circles: referral groups of 3–5 friends or family. When the group keeps a shared cumulative deposit threshold, they unlock:

- Better interest rate

- Group experiences (e.g. tickets, concierge moments)

- Priority service for the entire group (as the group now becomes a unified client in the bank’s data warehouse)

Now deposits don’t just earn interest. They earn shared experiences and belonging. At its core, unreasonable hospitality is designed to convert trust into sticky deposits by making clients feel at home—and by making the bank their primary bank.

E: “Wow Moments” That Anchor Loyalty

From the book’s 95/5 rule, unreasonable hospitality dedicates 5% of CAC or annual profits to surprise-and-delight moments that build long-term retention. But not randomly.

Unreasonable Hospitality’s Motivation Engine (I wrote about it in my previous articles, but one needs to do a psychological profiling to utilize its benefits) uses behavioral signals and contextual events to personalize:

- A Spotify/Netflix/eSIM subscription after paying off a loan.

- A flight voucher when you finish your school.

- A random card fee waiver before your trip.

- Cleaning service subscription after you’ve bought your first house.

This isn’t marketing. It’s scalable hospitality that directly reduces churn and builds emotional affinity.

F: Hospitality Studios and Outposts

Step away traditional branches. Launch and operate modular studios/lounges/pods in airports, university campuses, train stations, retail centers, coworking spaces—where people already go. No massive capex. Just presence, conversation, and onboarding power.

Think: banking meets hospitality lounge.

G: Better Way to Onboard: From KYC to Life Story

During on-boarding, you ask:

“What’s a money moment you’re proud of?”

“What do you want money to do for your life?”

You still snap the ID. But you also build a profile rooted in goals, not just compliance. This drives the app’s interface, your concierge relationship, and your upgrade eligibility.

H: Surprise Upgrades & Moments That Matter

Unreasonable hospitality monitors life signals:

- Job changes

- Health issues

- Relationship milestones

And acts without you asking:

- Pauses fees after job loss

- Suggests insurance when you become a parent

- Boosts your credit line with a note: "We believe in you."

I: Beyond Deposits: Emotional Bancassurance & Wealth

Insurance and investing often feel cold. Unreasonable hospitality humanizes them:

- New parents get jargon-free life insurance journeys.

- Regular savers unlock investing tools (investing app cost coverage) with real education.

- Burnt-out earners get access to wellness-linked products for free.

Every product asks first: "How does this make our client feel safer, stronger, more seen?"

J: Metrics That Matter: Feel Ratings

Every touchpoint ends with a Feel Rating:

- Made me smile

- Solved my need

- Lifted my mood

- Left me cold

Not vanity metrics. They’re emotional KPIs tied to retention and advocacy.

Final Thought: Trust Is the Cheapest Deposit

In a world drowning in CAC and digital churn, emotional loyalty is the rarest, most enduring asset.

Hospitality isn’t fluff. It’s strategy. And when clients feel at home - when their money is treated with care - they’ll stay. Even at the account of cheaper competitive offering.