< GO BACK

The Greatest Risk in Traditional Banking

March 17, 2026

/

GENERAL

Picture a small boat on a restless river. The current pushes forward, but conditions shift faster than the crew can adjust. Rocks appear, rapids break out, newly adapted predators swim around and sometimes the riverbed itself dries, demanding the boat transform to survive. Around them, much larger boats cut through the same waters — they have more men, more ammunition to fight predators, more steel to re-shape when needed.

It’s the smaller boats that carry the greatest risk. For them, every wrong turn could be existential. With limited size and thinner crew, they don’t have the luxury of drifting or waiting for calmer waters. If their captains lack vision or move too slowly, the boat finds itself pushed to the riverbank, stranded.

This river is today’s banking environment — disrupted by technology, shifting customer behavior, and macroeconomic change. New wildlife appearing everywhere are the challenger & neobanks & fintech players, and the boat sizes depict vast size differences within the traditional universal industry players. The changing picture of the entire landscape where the river flows is the great banking transition. And it doesn’t test everyone equally. For many small, traditional banks — the sub-scale players that still dot markets across Europe — the very viability of their operating business model is at stake. As the river itself does not resemble well-watered Amazon anymore, it’s more like unpredictable Zambezi now.

Banking Risk: The Basics

Banking is all about risk – return mitigation, with numerous and increasingly fast evolving mitigation techniques being part of its business model since the inception. Banking evolves rapidly. Business models that were viable just a decade ago are often obsolete today. Sophistication has increased dramatically across every core vertical, demanding faster adaptation and deeper expertise. To simplify, banks make, lose or forgo returns by managing several core groups of moving target risks in parallel: credit risk (“who you lend or place the money with”), liquidity risk (“how you gather and place funds given that both sides of the B/S constantly move”), interest rate risk (“at what prices you lend and borrow”), market risk (“currency and equity/leverage price moves”), capital management risk (“how you manage complex capital allocation”), a whole bunch of operational & IT risks (“risks stemming from fast-paced technology development, cybersecurity being on top of that group”) and even ESG risk (“brought forward by climate awareness and regulatory sophistication increase”). Not exactly a walk in the park, the business requires specific and deep know-how domains to call the right shots.

Now combining the banking business risks, the changing business environment and the fear of loss[1] theory, we come to the risk of business viability which increasingly looms over the long tail of smaller banks which have historically existed across the various developed or fast emerging markets and still make up an important part of the sector.

The Greatest Risk of the Sub-Scale Banking Business Model

What is a sub-scale bank? In my mind, that would be a universal incumbent (traditional) bank with up to ~EUR 2bn (or less) in asset size which commands less than 5% market share where it banks today. Across my SEE region, expanded with Romania, Bulgaria and Albania, there’s ~100 of banks that fall within these limit ranges. And these are operating across frontier/emerging market landscape. Applying these criteria to the Eurozone, including co-ops and savings banks (i.e. German small “sparkassen” banks), we get a number of ~1.000 banks[2]. Each with their own retail, micro and SME corporate clientele, each doing business within their own geo niche, sometimes as small as the single small city. Their brand power doesn’t stem from a product, instead, if they are good, it lies in the superior client service (rarely), deep-rooted historical clientele stickiness or simply very limited local competition. But the fast-expanding banking ecosystem is pushing both their products and services out of their “catchment zones” as digital technology makes geo presence less of a factor even at intra-market scale. Technology disrupts banking habits and changes the behavior patterns with the clientele, making chasing both client loyalty and new client acquisition harder for the unspecialized players without larger capital backing (i.e. like with subsidiaries banks) to invest into size, tech and brain. The Greatest Risk is therefore a survival risk, no less, no more.

The Importance of Size in Banking

Like in any industry, business size always plays a role, but banking is somewhat different here, as your key product is essentially a commodity, sold in 1.000+ packages, tailor-made or off-the-shelf type. The “quality of the product” doesn’t even slightly differentiate like it does across the commodities industries, the main differentiation points are “the structure and complexity of packaging” (justifying price differences) and client service (with speed-to-serve and cost-to-serve playing increasingly key roles here).

Now let’s see how the great banking transition elements and trends[3] impact the banking sector and why size impacts the risk profile. We namely know that the great banking transition is happening across three battlefields: 1.) Balance sheet to off balance transition, 2.) Distribution power shifts and 3.) Changes and advances across the transactions & payments ecosystem.

Super-simplifying, what do these three battlefields imply from the “boat size” perspective:

Transition of Funds into Off Balance Sheet domain

In search of higher returns, sophisticated client funds have been growing and migrating out of the banks’ balance sheets - away from corporate and retail deposits, bank bonds and other liabilities - and into nonbanks, into off-balance-sheet vehicles such as pension funds, digital assets, private capital, private debt, and other institutional alternative assets under management. Not necessarily riskier, but surely less regulated. This shift has been occurring across most geographies, however most of the smaller sized banks barely felt it, due to client structure. During last 10 years, more than 70 percent of the net increase in financial funds went into off-banking balance sheet, although banks’ balance sheets have also been growing, but at much slower pace. And this trend is irreversible. Funds growth has been transitioning away from bank balance sheets due to two reasons: more attractive risk-return balanced propositions outside of the core banking sector and more tailored client service.

Example: The indicational global split of funds between B/S and off B/S

Traditional universal banking regardless of size is balance sheet and capital heavy business. It generally profits when rates are rising and NIMs increasing under normal structure of the liabilities side of the business (mostly deposits). When the rates are falling or we have a stable, flat rate environment (the period we are experiencing for some time and is unlikely to reverse mid-term), the size of the balance sheet becomes way more decisive factor for banks which want to exemplify a clear business case of long term profitable growth, both on risk-adjusted basis (acknowledged by P/B ratios) and topline / bottom line growth basis (acknowledged by P/E ratios) transformation path.

Let’s further look at where the bank’s revenues come from (picture below): appx 60% comes from lending (where the distribution power and technology factors play an increasingly important role, especially with retail), the rest is mostly scale and fee-driven expert know-how business within transactions and AUM management domain. Both under heavy “attack” by specialists with less capital heavy balance sheet model. Furthermore, the nonbank fund providers already account for more than 14 percent of all the global lending, and this % is rising.

Why is scale becoming a decisive factor for banks trying to catch the B/S to off B/S wave:

- For larger B/S traditional banks the capital is easier to get optimized for off-B/S transition, the key players in the off B/S world will unlikely co-operate with sub-scale banks.

- Fund pools which are off B/S are not accessible to sub-scale banks without clear specialization.

- Most profitable product stacks in today’s traditional banks’ corporate portfolio (i.e. trade finance products…) or the tactics to even unbundle part of the balance sheet (by originating and distributing loans but funding them via 3rd party source or securitizing them) are less accessible to sub-scale banks, as clients need size.

- Technology shifts and advances, coupled with talent superiority are dominating payments and asset management space, while investment banking and infrastructure development have mostly been out of reach for smaller bank players.

- Last but not at all least, the funding side (deposits) costs, determining the “passive margin” component of NIM, are under increased pressure (rising costs) if your bread and butter are plain vanilla loan products distributed under non-highly appealing brand.

Distribution power shifts

Within lending propositions, distribution models are changing rapidly; fully digital and embedded finance models redefine client acquisition.

- Sub-scale banks cannot win the distribution power game unless they follow the path of digitally native players (facing serious know-how and IT limitations, as their core business model is simply not made to be digital-first or digitally native).

- Technology adoption is now a survival factor: while generative AI, automation, process streamlining and cloud migration can cut costs by 10%–20%, they require up-front investment and expertise: money and brain in other words. Small banks have limited capex generation pool. Unless their future operating model is aimed to serve sub-prime clientele at the account of higher cost of risk, their appeal with the future digitally focused retail clientele will diminish.

- Lagging in tech will inevitably lead to weaker customer experience, higher fraud exposure, higher future costs, not to mention that genAI models are becoming the competitive edge in modern risk underwriting as well.

- Without partnerships, small banks risk losing primary relationships, as their existing client base ages.

- Their ability to efficiently distribute and competitively price plain-vanilla products is also decreasing (if long term profitability growth is taken as the key metric), complex higher value products or adjacent embedded finance ecosystem products are out of reach, unless supported with higher IT capex and extreme client centricity culture.

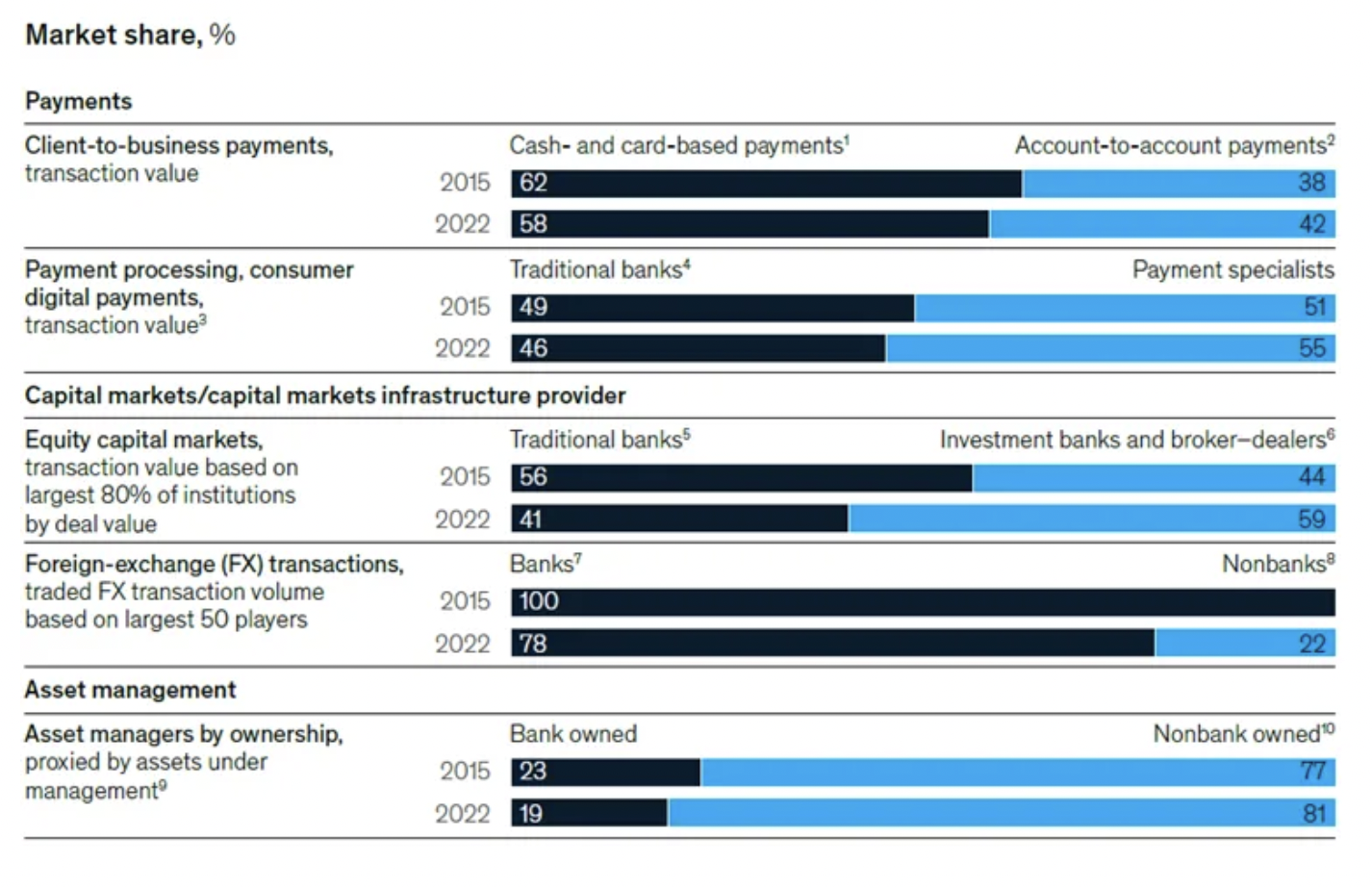

Transactions ecosystem is more penetrated with specialists than any other

New business models are reshaping transactions ecosystem super quickly, and irreversibly, being in the FX, trading platforms, remittances, crypto, payment processing, merchant acquiring. Market shares held by traditional banks in these segments are falling at accelerated pace, faster now vs already depicted by below chart showing 2015 – 2022 trajectory. And most of today’s fintech unicorns come from this space.

- While larger banks try to keep up with pace due to still prevalent market positions, technology capex, talent acquisition capacity, and geography shields (i.e. in some markets of my region Apple Pay literally just entered the market, while Revoluts and alike are still not there), sub-scale banks are exposed.

Future Scenarios for Sub Scale Bank Business Models

Adding to the above-described battlefields, brought forward by the great banking transition, there is one more drag on the business model of a small banking boat, and that’s regulation: regulatory and risk burdens weigh disproportionately on smallest players - Basel III and AML compliance costs weight heavier as % of revenue. Digital Euro will also erode the deposit base. Limited specialist risk capacity increases exposure to shocks. Like if the new Zambezi landscape would not be enough.

With cost cutting alone, you cannot sustain long term profitability, because banking has a leveraged business model and cannot simply just cut costs to maintain profitability. Because profit uptake (NIM related) curve has reversed and without topline growth (dependent on growing loan and deposit book in parallel, and dependent on growing fees, also outside the B/S) you erode value of capital and small banks are prone to do that faster than the larger ones if not reinventing the operating model

Here are some mid-term future scenarios for sub-scale banks my imagination came up with:

Final word: Management IQ will be the determining factor. For many sub scale banks, there are limits to what can be done structurally (like shifting geographies and entering more attractive lines of business). It will be hard to find scale where it matters.

Success in this transition demands bold, disciplined leadership. Management must demonstrate strategic vision, humility, and a willingness to learn fast. Execution excellence, supported by focused investments in scale, technology, and talent, will ultimately separate the survivors from the rest.

I suggest Nickleback’s song “What are you waiting for” playing in the background for the motivation.

[1] Good read (somewhat theoretical): »Fear, Not Risk, Explains Asset Pricing; Arnold, McQuarrie; Feb 2025

[2] Source: Collated reports by Central banks, with several intra market assumptions, 2023-24

[3] The Great Banking Transition: McKinsey, October 2023